First Nations Finance Authority (FNFA) Issues its Largest Bond to date.

Westbank, British Columbia (October 28, 2019) – The FNFA has issued its sixth debenture into the capital markets, raising $170 Million for 22 First Nations. The debenture was purchased by institutional investors both domestically and internationally. This brings total debenture issuance by the FNFA since 2014 up to $678 million.

FNFA’s debentures are backed by its First Nations’ “own source revenues” which are stable, predictable revenue streams that are generated by each First Nation.

“The confidence shown to FNFA by investors in the capital markets continues to grow,” explains Ernie Daniels, President and CEO. “The infrastructure and economic development that FNFA First Nations have undertaken have created an estimated 1,484 new jobs this year, most of which were on reserve lands employing First Nations people. Every FNFA loan is a success story, and we are very proud to play a role in our members achieving their community priorities. The economic impact of these investments benefits all Canadians.”

The purposes for which the sixth debenture proceeds were used include such projects as multi-purpose administrative buildings, business parks, two large hotels, business acquisitions, a school addition/renovation, commercial travel centres, land developments and a hydro power development.

“The FNFA continues to make a positive impact in the First Nations. This membership now extends across 8 provinces and one Territory,” states FNFA Chair Chief Warren Tabobondung of Wasauksing First Nation. “The mandates under our Act not only creates access to government-rate loans and repayment terms through the FNFA, but also a pathway to enable communities to strengthen their internal capacities with the goal of applying best practices to managing our own wealth and future opportunities. First Nations are coming to the realization that we are stronger together. We are taking control of our own futures by accessing capital and developing our own communities on our own terms.”

FNFA membership is open to all First Nations across Canada, and is governed by its members.

For More Info:

Ernie Daniels President and CEO First Nations Finance Authority PH: (250) 768-5253 Fax: (250) 768-5258 info@fnfa.ca

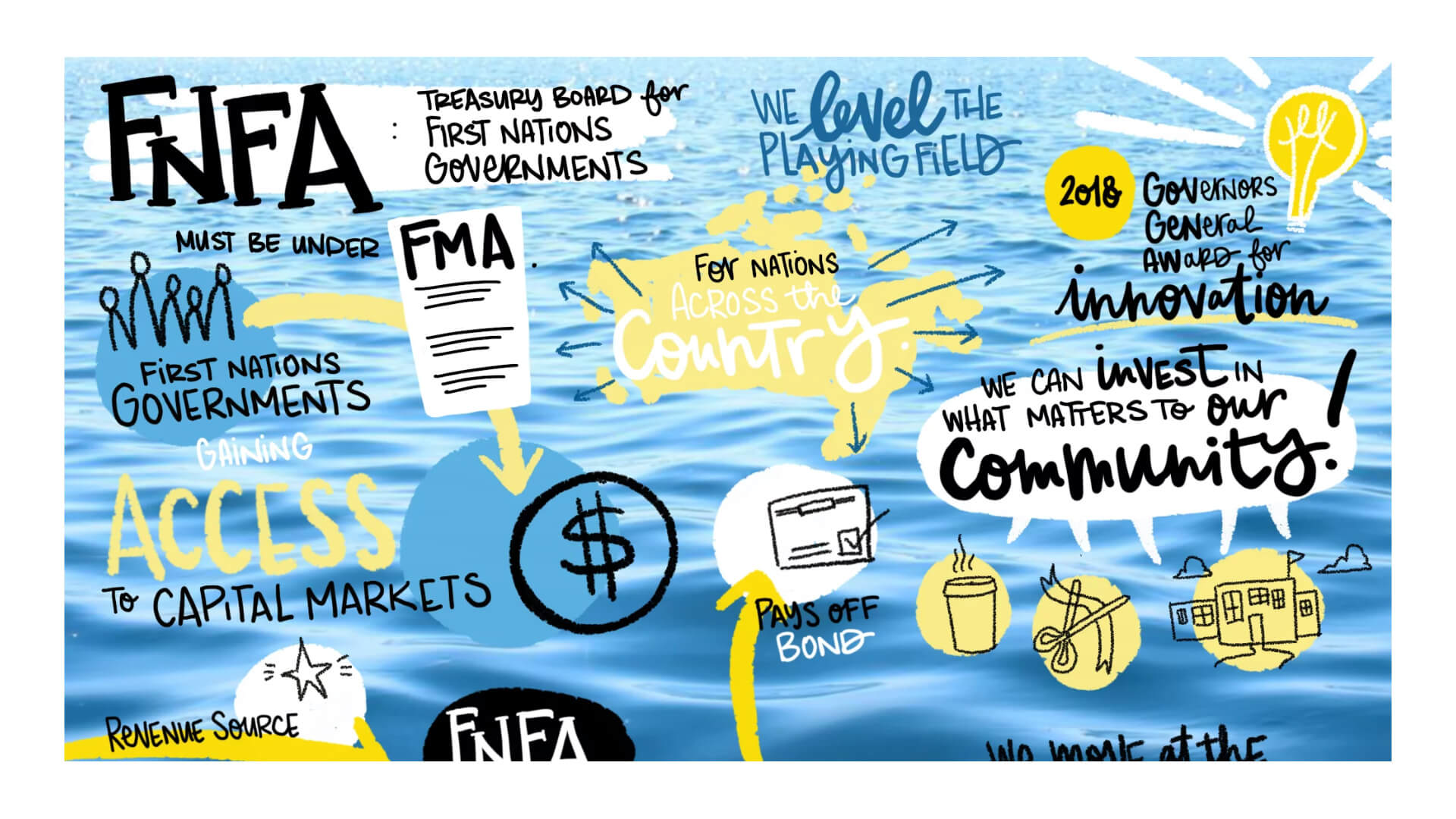

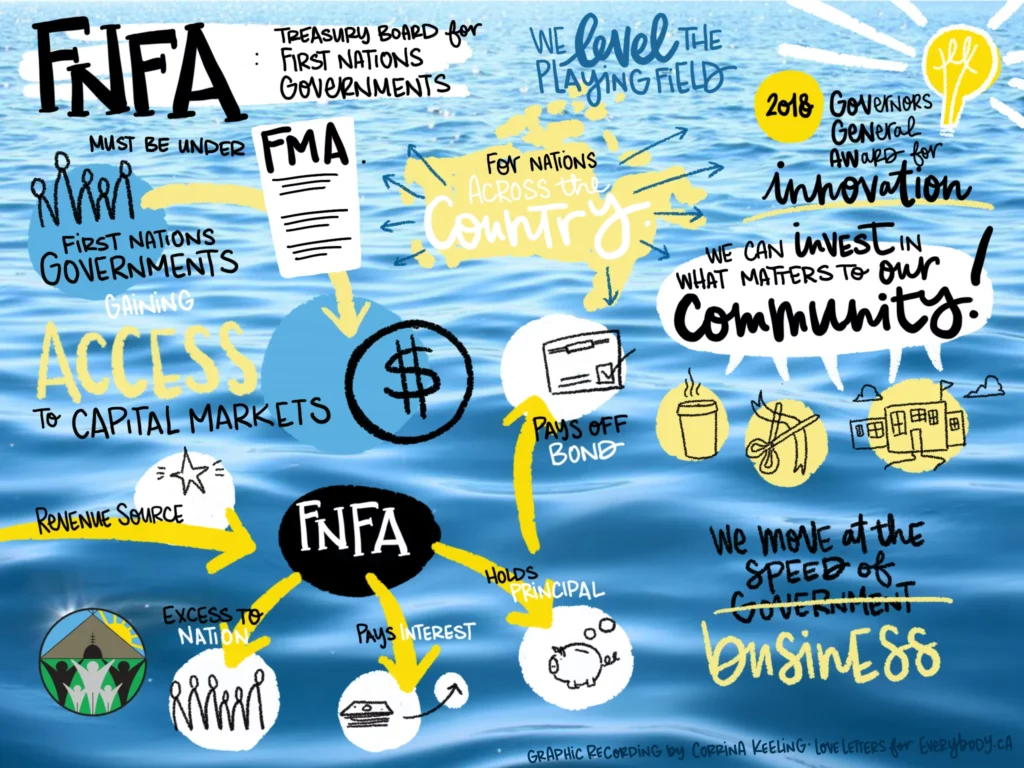

The FNFA is a not-for-profit First Nation institution established pursuant to the federal First Nations Fiscal Management Act, that provides any qualifying First Nation from across Canada with access to the capital markets. The First Nations govern the FNFA, as members elect from amongst themselves a Board of Directors.

FNFA facilitates loans to Borrowing Members from the proceeds of bond issuances. These loans can have repayment terms up to 30 years and offer fixed-rate options to assist the member First Nation’s budgeting needs. In order to fund member’s borrowing requirements prior to an expected bond issuance date, the FNFA also offers short-term loans at below Bank Prime. Short-term loans are rolled over into each new bond. As more First Nations qualify to become Borrowing Members, the FNFA will continue to grow and diversify, looking to strengthen its credit rating and consequently the financial benefits to its members.

New report aims to give clearer picture of Indigenous impact on provincial economy

Source: Cameron MacLean · CBC News · Posted: Jan 10, 2019 3:00 AM PST | Last Updated: January 10, 2019

Indigenous people in Manitoba pump billions of dollars to the provincial economy each year, according to a new report that aims to give a clearer picture of the economic impact of First Nations, Métis and Inuit people.

Total spending by Indigenous governments, businesses and households in the province added up to $9.3 billion in 2016, says the report — a collaboration between Manitoba’s Southern Chiefs’ Organization, Manitoba Keewatinowi Okimakanak and the Rural Development Institute at Brandon University.

“It’s the first of its kind, in which we have a pretty accurate analysis of the kind of contributions that Indigenous people are making to the economy,” said Southern Chiefs’ Organization Grand Chief Jerry Daniels in an interview with CBC’s Manitoba’s morning show, Information Radio.

The report looked at Indigenous economic impact in four categories: gross domestic product (a measure of the total value of goods produced and services provided in the province), employment, labour income and taxes paid.

In 2016 alone, the Indigenous economy added $2.3 billion to the provincial gross domestic product, the report found.

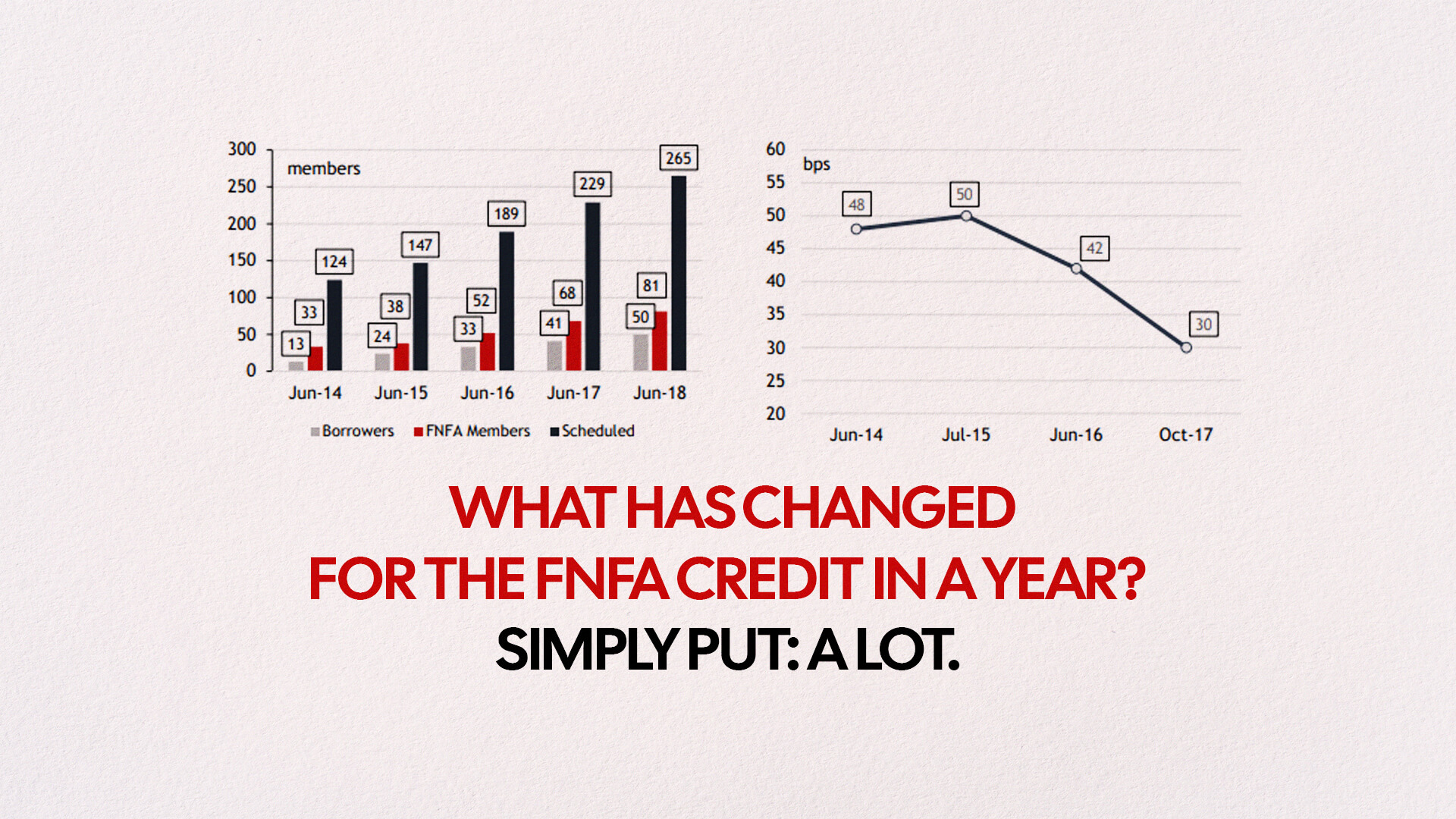

It’s been almost a year now since the First Nations Finance Authority last came to the market on October 19, 2017, having issued $126 million of its 3.05% Jun-2028 at 107 bps vs Can 1.00% Jun-27, representing 30 bps over Ontario at the time. With new indications hinting that the name could return to the market for a fifth time in the near future, one can’t help but wonder: what has changed for the FNFA credit since then? Simply put: a lot.

Bloomberg Ticker: FNFACA First Nations Finance Authority (‘FNFA’ or ‘Authority’) was built on a robust planning framework that spanned more than 20 years in development. The process originated with meticulous federal government policy research, and eventually led to the enactment of supportive and protective legislation that underpins sound financing practices. This framework ensures the utmost protection for bank lenders and bondholders. The framework establishes clear parameters which gives First Nations communities access to capital for important infrastructure and business development.

Canada’s First Nations have made strong progress over the past decade in securing their entitlement to share in the financial benefits of Canada’s natural resources, and asserting their rights to be consulted on major energy and resource projects. First Nations and Canadian government relations at all levels are being re-set on a course of stronger understanding and cooperation to secure a brighter and better future for all Canadians. To this end, FNFA is an important funding platform that harnesses the capacity of the institutional capital markets to participate in this journey. There are currently 200 First Nations out of 634 across Canada scheduled in the program. FNFA projects its loan program to grow from approximately $297mln today to over $1.2bln by 2021.

“Resetting the relationship and affirming First Nation rights and First Nation government responsibilities to their people can unlock economic potential, and generate significant and essential opportunity for all Canadians,” stated Shawn Atleo, former National Chief of the Assembly of First Nations.

Dr Dominique Collin is a former senior economist with the Government of Canada (Department of Indigenous and Northern Affairs Canada, or ‘INAC’), and is now Principal of Waterstone Strategies, a private consulting firm.

A quote from Dr Dominique Collin: I have been involved in Aboriginal access to capital issues for 30 years, from the federal government side and from the Aboriginal financial institution side, and in all that time I have not come across any instance of First Nation governments defaulting on long-term infrastructure or public work-related debt. Social housing debt, the single largest block of First Nation government debt, has been an important feature of First Nation government finances for more than a generation, most of it with federal government backstop. The published loss rates for government housing backstop programs are close to nil, as confirmed by a sequence of Auditor General reports on Aboriginal housing, confirming that First Nation governments are a good lending risk. Over the past 10 years, a rapid increase in own-source revenues from benefit agreements, royalties, revenue sharing agreements, participation in major energy, and resource projects has multiplied the capacity of First Nation governments to address business and infrastructure investment needs with debt. Setting aside community-owned business ventures, which on the whole have done well but remain within the business risk category, I am not aware of any defaults. This likely results from the solidity of the revenue streams used for borrowing, the increased ability of lenders to understand the lending environment and, most important, from the willingness of revenue-rich First Nations to opt into rigorous financial administration oversight regimes such as the one provided by the First Nations Financial Management Board certification process.

Dr Collin has been involved in a number of Aboriginal financial institution development initiatives in the areas of business, infrastructure and housing finance. He is the coauthor, with Michael Rice, of Access To Capital for Business: Scoping out the First Nation and Inuit Challenge, an in-depth analysis of Aboriginal access to capital performance and issues from 1975 to 2003. An update of this report to 2013, with an analysis of the 10-year increase in outstanding business/infrastructure debt, will be published in the fall of 2016.

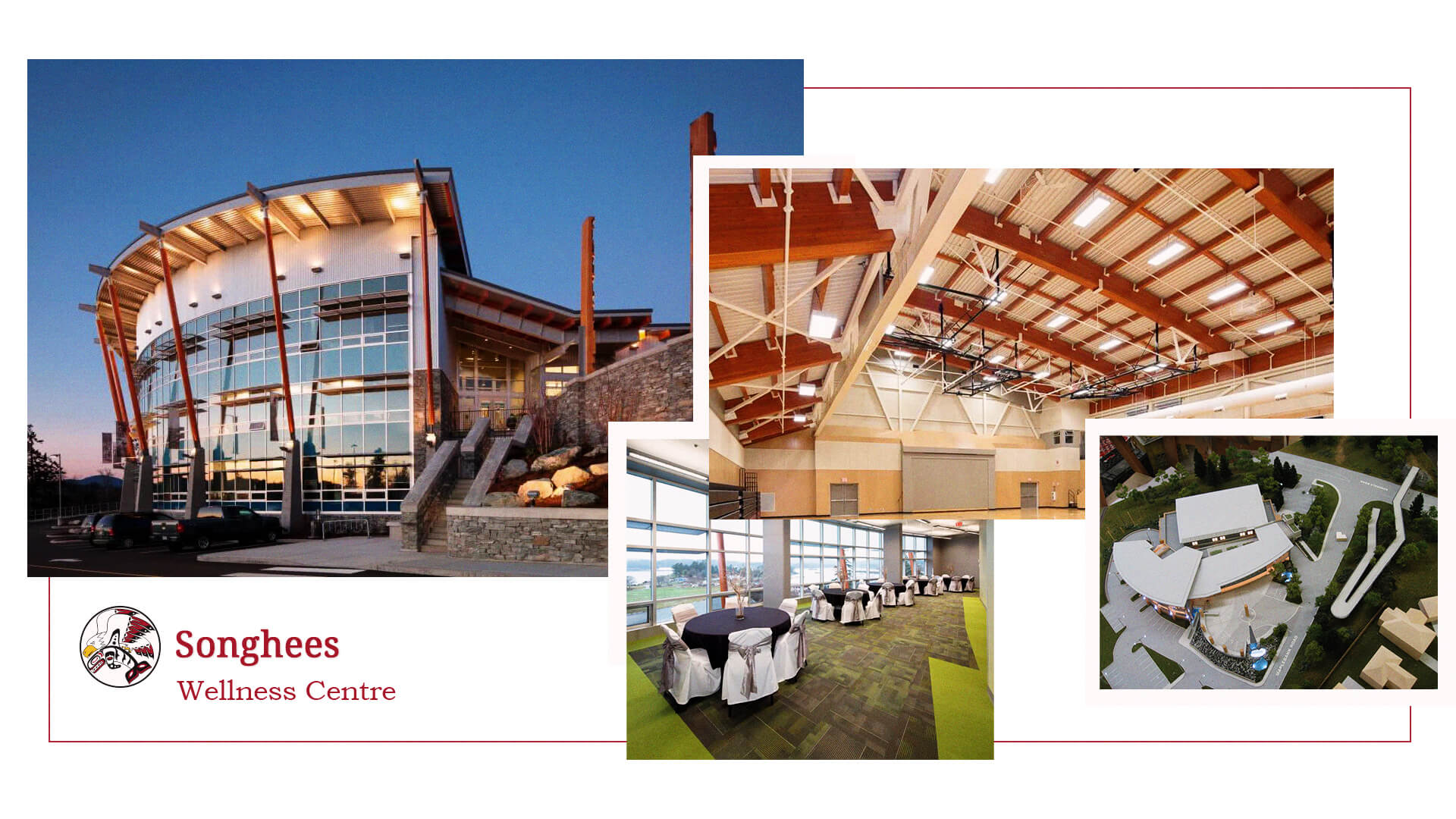

An example of an FNFA loan is the $5.27mln, 30-year term loan to fund the Songhees Wellness Centre in Victoria, British Columbia (shown below), which is backed by a federal 20- year Right-of-Way contract giving a Canadian naval base road access through lands owned by the Songhees First Nation.

The Songhees Wellness Centre, Victoria, British Columbia

Topics Covered, by Section:

Debt Issuance, Valuation and Portfolio Placement

Legislative Framework, Lending Approach and Bondholder Protections

Credit Underwriting Process and Experience

Financial Reporting and Transparency

Canada’s Political System and First Nations

History of Canada’s First Nations

Debt Issuance, Valuation and Portfolio Placement

First Nations Finance Authority FTSE TMX Canada Universe Bond Index Classification

Sector: Government

Industry Group: Municipal

Industry Sub-Group: British Columbia

Rating: A

Index Weight: Less than 0.5% Regulatory Classification:

Basel III Risk-Weighting – Standardized Approach*: FNFA is a non-share, nonprofit corporation and may meet the criteria for a ‘Claim on Corporate’ with a credit assessment rating of A- to A+. Under this criteria, bonds would be subject to a 50% haircut. Investors are advised to consult their legal counsel.

HQLA – OSFI Liquidity Adequacy Guideline/Basel III: FNFA is a non-share, nonprofit corporation and may meet the requirement of a Level 2B asset (50% haircut). Investors are advised to consult their legal counsel. *FNFA is not classified as a Public Sector Entity (PSE) for purposes of the Capital Adequacy Guidelines. Chapter 3.1.3 of the guidelines provides that where PSEs other than Canadian provincial or territorial governments provide guarantees or other support arrangements other than in respect of financing of their own municipal or public services, the PSE risk weight may not be used. The PSE risk weight is meant for the financing of the PSE’s own municipal and public services.

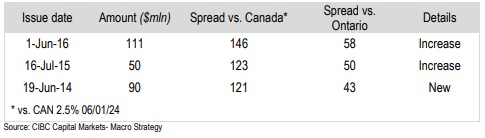

First Nations Finance Authority began funding in the institutional debt markets in June 2014 with its inaugural 10Y issue of $90mln (FNFACA 3.4% June 26, 2024). Since 2014, the Authority has tapped the market once a year by upsizing the existing issue twice. Going forward, FNFA is planning to continue targeting the 10-year funding area. It expects to issue $130mln annually for next two fiscal years as the client base increases. In the third fiscal year, it anticipates doing both spring and fall issuances, aggregating about $250mln in each fiscal year.

Like other government issuers, FNFA raises debt in the exempt market by offering securities via an Information Memorandum. The Authority has historically borrowed through a syndicated market process. There are 20 to 25 investors currently participating in FNFA’s debt issues, crossing all investor types. While the majority of investors fall into the category of large Canadian institutionals, there has been a modest level of Canadian retail participation. There has also been a good level of participation by US investors. The most recent transaction was distributed to 22 institutional investors, with an overall blend of almost 50/50 between repeat and new, as the investor base continues to grow.

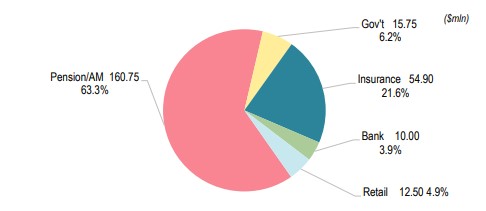

Debt Issuance by Type

Source: FNFA, CIBC Capital Markets – Macro Strategy

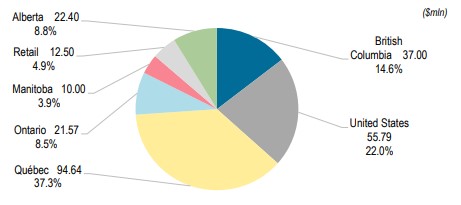

Debt Issuance by Location

Source: FNFA, CIBC Capital Markets – Macro Strategy

FNFA bonds are classified in the FTSE TMX Canada Universe Bond Index in the Municipal sub-sector category. Like other Canadian bonds in this category, FNFA bonds are best suited in investment portfolios as ‘buy-and-hold’ positions in passive mandates, as well as a component of active mandates. They also have broad appeal in retail accounts due to their investment grade quality and name familiarity. FNFA bonds may also be suitable for holdings by regulated financial institutions.

The municipal sub-sector represents about 2% of the FTSE TMX Canada Universe Bond Index, and we are constructive on a ‘modest’ overweight position (3-4%) at current spread levels, and a position in FNFA bonds towards an overweight.

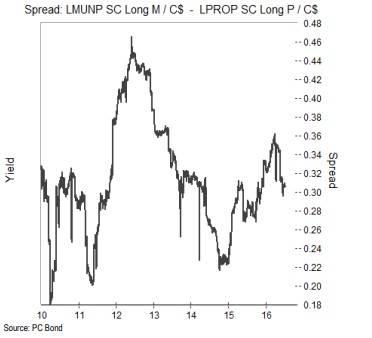

In spite of the generally stronger credit risk profiles of municipal bonds, these types of bonds trade back of their more senior provincial counterparts and generally move in tandem. As depicted in the spread graph below, earlier in the year, municipal spreads moved wider than their provincial counterparts (i.e. basis risk) reflecting a global re-pricing of liquidity premiums that was spurred by extreme market volatility and risk aversion. Spreads have since tightened somewhat, but the liquidity spread premiums remain attractive in the current low interest rate environment where investors are searching for yield.

It’s important to highlight that secondary market liquidity continues to be impinged upon by regulatory requirements imposed on financial institutions and their broker/dealers. Moreover, a trend towards dealer inventory aging requirements is also having an impact.

Long Muni Index Spread over Long Provi Index

We like FNFA municipal bonds as a means to anchor portfolio credit quality (Moody’s A3, Standard & Poor’s A-, all outlooks ‘stable’) and for yield pick-up. We expect FNFA’s credit risk profile to be relatively stable, and improve over time.

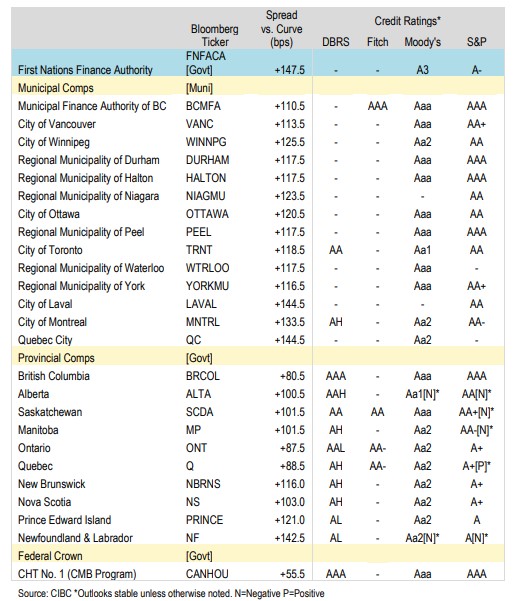

10Y New Issue Indicative Bond Market Comparables

FNFA’s credit ratings are predicated on several factors. These factors include the strong institutional and legislative framework, the expectation that FNFA is likely to receive extraordinary government support, a solid governance and management structure, a rigorous credit review process, strong interest and debt service coverage ratios, and several structural protections that include:

A mechanism to intercept revenue streams (‘Other Revenues’) that secure a Borrowing Member’s loan payments and the deposit of these revenues, either directly or by an intermediate account, into a segregated trust account (a ‘Secured Revenues Trust Account’);

A Debt Service Reserve Fund (DRF) that is funded by a hold-back of 5% of the loan advance, which serves as a layer of cross-collateral protection. Recent changes to the First Nations Financial Management Act, FNFMA, now permit the holdback to vary between 1-5%, but Management’s intentions are to stick with the practice of 5%. (Additionally, rating agencies will be consulted ahead of a change, as the FNFMA provides that the FNFA’s Board can only permit a lower hold-back if there are no adverse rating consequences.). There is a requirement to replenish the DRF on a ‘joint and several’ basis among all Borrowing Members who received financing from the FNFA, but only within each borrowing stream (i.e. Property Taxes or Other Revenues);

A $10mln Credit Enhancement Fund (CEF) that was funded by the federal government. The CEF was established to enhance the FNFA’s credit rating by being available to temporarily offset any shortfalls in the Debt Reserve Fund. The CEF will be increased to $30mln within the next year with a $10mln instalment this fall and another $10mln instalment next spring; and

A legislative requirement to establish a sinking fund for each bond issue, which builds based on the amortizing structure of the underlying loan.

The presumption of extraordinary federal government support is reasoned on the fact that it is highly embedded in the overall program. The federal government has played an integral role in establishing the framework for the FNFA through the enactment of federal legislation, the establishment of federally operated boards engaged in processing First Nations community groups into the program, ongoing oversight thereafter, and the provision of funds for the Credit Enhancement Fund. With respect to the latter, the recent Federal budget explicitly mentions ongoing intentions to build a better future for Canada’s Indigenous Peoples through a wide range of initiatives as well as support for the First Nations Finance Authority to provide $20mln over two years, beginning in fiscal 2016-17, to strengthen the Authority’s capital base.

While there is no explicit federal guarantee on FNFA bonds, the aforementioned factors add up to a strong level of implicit and explicit support.

FNFA offers its borrowing members two types of loan facilities: Interim, and Long-Term Loans. These facilities are discussed in more detail below. FNFA finances these loans through a syndicated Bridge Financing Facility (the ‘Facility’) with three Canadian chartered banks until it arranges long-term funding through a debenture offering.

The Facility is secured by first-ranking liens on all real and personal, corporeal and incorporeal, present and future assets, including on all of the accounts of FNFA (including accounts that hold the CEF and Debt Reserve Fund) and the rights of FNFA in the Secured Revenues Trust Accounts and the Property Tax Accounts. FNFA is subject to non-financial covenants, including a Material Adverse Change Clause and the ratings dropping to outside of investment grade. The credit facility also requires the maintenance of two ratings, which indirectly provides protections to bondholders as the debentures do not contain this provision. Since inception of the Facility, there has never been a breach.

In February 2016, the security rankings of FNFA’s debentures were upgraded to rank pari passu with FNFA’s $130mln secured line of credit. This was a major enhancement for bondholders.

We note, however, that FNFA’s ratings are constrained by a number of rating factors which are expected to abate over time. The rating agencies have cited FNFA’s relatively high – but declining – volatility in profitability (previous losses from one-time start-up, and lower federal grants and management fees), the geographic concentration of borrowers in the province of British Columbia, which currently stands at 41% (July 2016), but is down from 65% in 2014, as well as its short operating history. An improvement in any of these along with a stronger liquidity profile could drive the ratings up. Conversely, a deterioration in the overall quality of the loan pool or change in the FNFA’s framework and/or structural considerations for the rating, including a reduction in government support, could put downward pressure on the ratings. We are not expecting any changes to FNFA’s credit ratings in the near term, but we believe there is more upside potential than downside risk to bondholders.

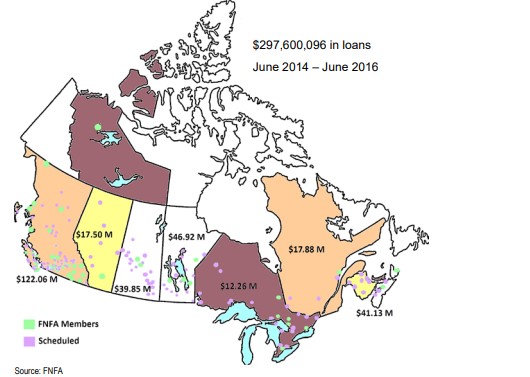

FNFA Borrowing Map

FNFA’s internal liquidity consists of approximately $2.2mln in cash and equivalents, $12.5mln in investments representing amounts held in the Debt Reserve Fund and $10mln in the CEF, which will grow to $30mln by next spring. Today’s level of internal liquidity of around $25mln is just under 10% of outstanding debt, which is considered adequate for the ratings, but low for higher rating categories. The liquidity metric will improve with additional deposits in the CEF. External liquidity consists of the $130mln Bridge Financing Facility.

All in all, liquidity is considered adequate given the conduit nature of the intermediation process where payments are intercepted from Borrowing Member revenue sources to service outstanding debt and, therefore, liquidity needs beyond what is necessary for servicing debt are minimal. Although FNFA’s borrowing powers are not restricted to providing loans to Borrowing Members and it could borrow to finance working capital, historically the FNFA has financed its operations through federal government grants and operating income from the spread between what it borrows and lends at. On the lending side, FNFA’s mandate is only to make loans to First Nations that have qualified as Borrowing Members.

In the past year, FNFA’s loan portfolio has grown from $140mln to $297mln, with an increase in members from 23 to 34. In a year’s time, based upon the current loan portfolio plus the expected disbursement of $130mln in additional loans prior to March 31, 2017, the DRF will accumulate to approximately $21.5mln and the annual interest liability will be approximately $12.4mln. With the CEF at $30mln, interest coverage will be over 4 times ($30+21.5/$12.4). The FNFA plans to submit a request for a further $20mln to the CEF to expand it to $50mln in 2017 in order to maintain the interest coverage ratio at or above four times coverage (target interest coverage). Both Moody’s and S&P rate FNFA according to their government-related entities methodology. With respect to S&P, the criteria falls specifically under Rating Government-Related Entities: Methodology and Assumptions, published March 25, 2015. S&P gives FNFA a two-notch uplift from its Stand-Alone Credit Profile, or SACP, rating of ‘bbb’ because it views the likelihood of FNFA receiving extraordinary government support as ‘moderately high’. In a sovereign downgrade scenario – which we are not anticipating – the methodology permits the Government of Canada rating to fall two notches (i.e. from AAA to AA), without impacting FNFA’s ratings (all else remaining unchanged).

Under Moody’s Government-Related Issuers Rating Methodology (October 30, 2014), Moody’s applies its Joint Default Analysis (JDA) framework to its analysis of Government Related Issuers (GRI) to explain the credit links between GRIs and their supporting central, regional, and local governments. This approach gives FNFA a two-notch uplift from Moody’s intrinsic Baseline Credit Assessment score of ‘baa2’ on a “strong likelihood of extraordinary support”. Moody’s framework incorporates the concepts of dependency and support which, in FNFA’s case, would also accommodate a multiple notch downgrade of Canada. The framework suggests a rating change only if Canada’s Aaa were to drop to A1, assuming everything else remains the same.

We caution that all rating agency methodologies are theoretical reference points and final ratings are subject to the adjudication of the rating committees, but the aforementioned analysis does suggest a strong degree of flexibility in a sovereign downgrade scenario.

Legislative Framework, Lending Approach, and Bondholder Protections

First Nations Finance Authority (the ‘FNFA’ or the ‘Authority’) is a non-share, non-profit corporation established under Part 4, Section 58 of the First Nations Fiscal Management Act (FNFMA, or the ‘Act’) which came into force on April 1, 2006. The FNFA is not an agent of Her Majesty or a Crown Corporation.

First Nations Finance Authority’s head office is in Westbank, British Columbia. It operates within the terms of reference embodied in the FNFA. It runs its operations from a single location with credit adjudication done in-house as well as externally through a network of advisors located across Canada.

The impetus for the development of the First Nations Finance Authority was based on government policy research that concluded that a large gap exists in First Nations/Inuit access to affordable private capital which is hindering their economic potential. This conclusion was reached following a study that covered data from 1975 up to and including 2003.

First Nations/Inuit business financing access levels, trends and gaps all point to historical over-reliance on insufficient levels of government contribution capital and growth stalled at the early expansion phases for both the small and mid-sized ventures for lack of an organic connection to market capital. Correcting the situation is urgent and will require innovative ways to engage market sources of capital beyond the limited leverage ability of existing sources of government help. From Access to Capital for Business: Scoping out the First Nation and Inuit Challenge, by Dr Dominique Collin, Waterstone Strategies and Michael Rice, Indian and Northern Affairs Canada, May 2009.

First Nations Finance Authority fulfills an important role in reducing this gap. To facilitate funding for First Nations communities, FNFA’s objectives are to monetize federal and provincial revenue agreements with First Nations as well as First Nation’s own-source revenues.

The First Nations Fiscal Management Act sets out the procedure for First Nations to become ‘Borrowing Members’ of the Authority and the requirements that must be fulfilled as part of the borrowing process. It also gives the First Nations Finance Authority the powers to secure financing for its Borrowing Members, and to issue securities.

In addition to facilitating access to funding for its Borrowing Members, the FNFA also sponsors a pooled investment fund program for its ‘Investing Members’. Two pooled funds are offered: the MFA Money Market Fund, and the MFA Intermediate Fund. The funds are operated and managed by the Municipal Finance Authority of BC.

It’s important to understand that participation in the FNFMA is optional. It was designed as an optional piece of legislation to promote the continued economic development of participating First Nations, but respecting their rights to self-government and self-determination.

While all First Nations have the authority to pass by-laws related to the taxation of land under the Indian Act, the FNFMA offers an alternative and rigorous authority for First Nations to collect property tax. By opting into the property tax system under FNFMA, First Nations are better positioned to promote economic growth and capitalize on solid business relationships, resulting in a better quality of life for community members.

The act enables First Nations to participate more fully in the Canadian economy and foster business-friendly environments while meeting local needs by:

strengthening First Nations real property tax systems and First Nations financial management systems

providing First Nations with increased revenue raising tools, strong standards for accountability, and access to capital markets available to other governments

allowing for the borrowing of funds for the development of infrastructure on-reserve through a co-operative, public-style bond issuance

providing greater representation for First Nation taxpayers

The process to initiate participation in the FNFMA is via submission by a Band Council Resolution to the Minister of Indigenous and Northern Affairs requesting that the band be added to the schedule of the FNFMA. The process takes four to six months from the time the Band Council Resolution is received, but recent amendments to the Act are expected to shorten and streamline the process.

The FNFMA framework is supported by the work of the First Nations Finance Authority (FNFA), First Nations Tax Commission (FNTC), and First Nations Financial Management Board (FMB). The FNTC provides regulatory support to First Nations’ property tax jurisdictions. The FMB sets standards for financial administration laws that it must review and approve as well as conducts certification reviews of First Nations’ financial management systems and financial performance.

An important protection to bondholders is that before a First Nation can borrow funds from the Authority, the First Nation is required to make a Financial Administration Law regarding its financial administration. The law must be approved by the First Nations Financial Management Board (the ‘FMB’), the independent board established pursuant to the Legislation, that reviews the law for compliance with the Legislation and the FMB’s standards. The FMB’s standards are intended to support sound financial administration practices for a First Nation.

A First Nation is required under the Legislation to obtain a Financial Performance Certificate from the FMB before it can become a Borrowing Member of the Authority. A Financial Performance Certificate will only be issued after the FMB reviews a First Nation’s financial condition to determine if it complies, in all material respects, with the FMB’s standards. These standards are comprised of seven financial ratios that are applied to the First Nation’s past five years of audited financial statements. The ratios are intended to measure financial capacity or risk of overall structural deficit; ability to meet short-term operating obligations; ability to generate sufficient annual cash flows to maintain operations; ability to maintain a sustainable level of capital investment; debt burden and overall insolvency; ability to manage and execute budgets; and, the efficiency and stability in collecting property taxes. These financial tests are intended to measure financial capacity or risk of overall structural deficit; ability to meet short-term operating obligations; ability to generate sufficient annual cash flows to maintain operations; ability to maintain a sustainable level of capital investment; debt burden and overall solvency; ability to manage and execute budgets; and, the efficiency and stability in collecting property taxes.

Financial Ratios

FMB examines the First Nation’s past five years of audited financial statements to assess the following 7 financial ratios:

Fiscal Growth Ratio (if a decline greater than 5% occurs, then test failed)

Liquidity Test (if a decline greater than 10% occurs, then test failed)

Core Surplus Test (weighted average EBITDA must exceed 5% of current revenues) 4.Asset Maintenance (maintenance/replacement must exceed depreciation)

Net Debt Ratio (EBITDA is equal to or exceeds 1.5 times interest expenses) 6.Budget Performance (actual expenses cannot exceed budget more than 15%)

Property Tax Collection Rate (prior 5 year average collection rate must exceed 95%)

A First Nation must also obtain a Financial Management Systems Certificate within 36 months of receiving financing from the Authority (other than interim financing). Also, the Authority will require such a First Nation to obtain a Financial Management Systems Certificate prior to providing any loans subsequent to the loans contemplated by that First Nation’s initial borrowing law. A Financial Management Systems Certificate is more encompassing than a Financial Performance Certificate and will only be issued after the FMB reviews a First Nation’s financial management system to ensure it is operational and complies, in all material respects, with the FMB’s standards. These standards are intended to establish sound financial practices for the operation, management, reporting and control of the financial management system of a First Nation.

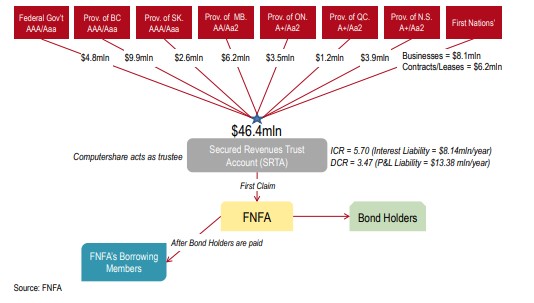

Claims to and collection of financial cash flows to service the FNFA’s debt is assured by several legal and structural protections.

Direction to Pay | Intercept The Authority uses a mechanism to intercept revenue streams (‘Other Revenues’) that secure a Borrowing Member’s loan payments. As required by the Legislation, each Borrowing Member irrevocably instructs third parties paying Other Revenues that secure a loan to pay those revenues, either directly or by an intermediate account, into a trust account (a ‘Secured Revenues Trust Account’) maintained by Computershare Trust Company of Canada (the SRTA Manager’) throughout the period of the loan. Under the terms of the Secured Revenues Trust Account, only the Authority (and not the applicable Borrowing Member) is entitled to instruct the SRTA Manager on the allocation and payment out of amounts from the Secured Revenues Trust Account and all payments to the Authority from the Secured Revenues Trust Account are made by the SRTA Manager. This ensures that amounts due to the Authority, including any amounts required to replenish the Debt Reserve Funds, are paid before any remaining amounts are paid to the Borrowing Member.

Intercepted Revenues Supporting FNFA Loans

Where the Other Revenues comes from a contract or an agreement, generally, the full amount of the Other Revenues is paid into the Secured Revenues Trust Account. Where the Other Revenues is from a Borrowing Member’s owned business, the amount collected into the Secured Revenues Trust Account is greater than that needed to fulfill loan payments. The Authority ensures the Secured Revenues Trust Account collections are equal to or greater than a debt coverage ratio. Each revenue stream is evaluated upon criteria such as payor risk, duration of stream, stability, etc. and has a debt coverage ratio applied to it.

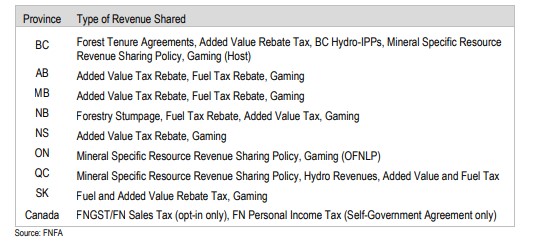

Revenue Sharing by Province

Priority of Claims

In the event that a Borrowing Member becomes insolvent, the Legislation (section 78) provides that the Authority has priority over all other creditors of the Borrowing Member (other than the Crown) for any amounts payable by the Borrowing Member to the Authority in connection with a loan secured by Other Revenues (as authorized under an agreement governing a Secured Revenues Trust Account) or under the Legislation.

The Authority does not rely on provincial Personal Property Security Act (‘PPSA’) legislation to perfect its security. To prevent inconsistent priorities, PPSA legislation generally excludes from its application security given by another enactment. Moreover, the Indian Act (section 88) provides that provincial laws of general application (such as PPSA legislation) are not applicable to or in respect of Indians to the extent that those laws are inconsistent with the Legislation.

Sinking Fund

The Authority is required by the Legislation to maintain a Sinking Fund to fulfill its repayment obligations for each bond issue. All principal repayments by Borrowing Members on loans from the Authority financed with proceeds of bonds are placed in a Sinking Fund for such bonds.

Debt Reserve Fund

The Authority is required by the Legislation, in connection with providing loans to Borrowing Members, to establish a Debt Reserve Fund. The Authority is required to withhold between 1% and 5% (the Authority currently withholds 5%) of the amount of any loan secured by Borrowing Members using Other Revenues and deposits that amount into the Other Revenues Debt Reserve Fund. If at any time the Authority has insufficient funds from Borrowing Members that have received financing secured by Other Revenues to make payments to bondholders, including Sinking Fund contributions, such payments are to be made from the Other Revenues Debt Reserve Fund.

If payments from the Other Revenues Debt Reserve Fund reduce its balance by 50% or more of the total amount contributed by Borrowing Members, then the Legislation provides that the Authority must (and may where the balance is reduced by less than 50%) require all Borrowing Members who contributed to the Other Revenues Debt Reserve Fund to pay amounts sufficient to replenish that fund. As a consequence of this replenishment mechanism, Borrowing Members that have received financing secured by Other Revenues are potentially liable for, and support, the debt obligations of any defaulting Borrowing Members that have received financing secured by Other Revenues. Amounts due to the Authority to replenish the Debt Reserve Fund may be drawn from the Secured Reserve Trust Account of a Borrowing Member, which collects an amount above what is required to service regular debt payments.

Credit Enhancement Fund

In accordance with the Legislation, the Authority has established a Credit Enhancement Fund of $10mln to support the Debt Reserve Funds in making payments to bondholders. This fund may be used by the Authority to temporarily off-set any shortfalls in the Debt Reserve Funds. On March 22, 2016, the Government of Canada, as part of its 2016 budget, announced that it proposes to provide $20mln over two years, beginning in the Government of Canada’s 2016- 2017 fiscal year, to strengthen the Authority’s capital base. Any such amounts received by the Authority from the Government of Canada will be added to the Credit Enhancement Fund.

Investment Authority

The Legislation provides that amounts in Sinking Funds, Debt Service Reserve Funds and the Credit Enhancement Fund can only be invested in certain eligible investments. The Authority may only invest in: (a) securities issued or guaranteed by Canada or a province; (b) investments guaranteed by a bank, trust company or credit union; and (c) deposits in a bank or trust company, or non-equity or membership shares in a credit union. With respect to Sinking Funds, the Authority may also invest in (a) securities of a local, municipal or regional government in Canada and (b) securities of the Authority or a municipal finance authority established by a province, if the day on which they mature is not less than the day on which the security for which the sinking fund is established matures.

The Authority has adopted a formal Investment Policy not to invest funds in a Sinking Fund for deposits in a trust company, or non-equity or membership shares in a credit union.

The Investment Policy has incorporated the following constraints:

DRF investments should attempt to provide sufficient liquidity through cash or cash equivalents to permit the FNFA to meet up to one year of sinking fund and interest payments for all outstanding debentures.

Sinking Fund investments should attempt to preserve capital and approximately match the debenture maturity date. However, it is understood that prudent investment management may entail some investments matching the loan term to the Borrowing Members instead of the debenture maturity term where these loan terms are for a longer period than the debenture (i.e. loans that will need to be refinanced over their term).

The Investment Policy has established guidelines with respect to credit quality and diversification.

Intervention Mechanism

If a Borrowing Member that has received financing secured by Other Revenues fails to make a payment to the Authority under a borrowing agreement, or fails to pay a charge imposed by the Authority in connection with replenishing a shortfall in the Other Revenues Debt Reserve Fund, the Authority can require the FMB to either impose a ‘co-management arrangement’ in respect of that Borrowing Member’s Other Revenues, or assume ‘third-party management’ of that Borrowing Member’s Other Revenues. If the FMB assumes ‘third-party management’ of the Borrowing Member’s Other Revenues, the FMB has exclusive right to, among other things, act in place of the Council of that Borrowing Member in relation to assets of that Borrowing Member that are generating Other Revenues.

In four years of FNFA loans, no third-party management or co-management arrangement has ever been initiated as a result of a Borrowing Member failing to make payments to the FNFA. It is highly unlikely in the future for any of FNFA’s clients since revenue streams are irrevocably intercepted for the full loan term from the payor source prior to loan release and the majority of these loans are payments from provincial governments or crowns. Hence, a failure in the intercept arrangements and/or a default of a province (or crown) would be a necessary scenario for this to happen. We highlight Canada’s strong AAA rating and the senior ratings enjoyed by Canada’s provinces. We also point out that FNFA does not have any single revenue stream clients.

In a revenue intercept scenario, FNFA staff would immediately contact the payor for an understanding. If the payor still refused to pay into the revenue intercept account with the SRTA manager, then a court action would be started.

The Financial Management Board, under the Legislation, has full authority to become the manager/treasurer over all of a Borrowing Member’s Other Revenues, including Other Revenues that currently do not secure loans by the FNFA. The FMB can use that authority to ensure amounts due to the FNFA are repaid. The FMB’s authority is under the Legislation, rather than contractual, which makes enforceability very strong. FMB staff do not do this intervention. FMB has an agreement with a national accounting firm that is an experienced intervenor to handle this function.

There is only one co-management arrangement existing in FNFA’s portfolio. The coarrangement is with St. Theresa Point, a band in Manitoba. The co-arrangement existed prior to joining the program. The co-arrangement was not related to failure to pay loan service or any liabilities, but rather related to the band asking for help in the areas of accounting and finance. The revenues servicing FNFA’s loan to St. Theresa Point are coming directly from the Province of Manitoba and the Debt Service Coverage Ratio (P&I) is strong at 6.28 times. The band is in a strong operating surplus position.

Recent Changes to the FNFMA

Legislative and regulatory amendments to the FNFMA came into force on April 1, 2016 stemming from recommendations and consultations with the FNFA, FMB and FNTC to improve the regime’s overall framework. The changes are expected to have a positive impact on facilitating entry of more First Nations, accelerate bond issuance and strengthen investor confidence. Notable enhancements include:

Allowing payments in lieu of taxation through a new fiscal power to collect fees for water, sewer, waste management, animal control, recreation, transportation and other similar services.

Giving First Nations the power to recover costs of enforcement, including the costs for seizure and sale of taxable property.

First Nations’ Financial administration laws must meet higher requirements set by the Financial Management Board (FMB) on an ongoing basis and these laws cannot be repealed unless they are replaced by laws approved by the FMB.

Tougher requirements on management of local revenues including their maintenance in separate accounts from all other First Nations moneys as well as separate financial reporting and auditing requirements, unless permitted by FMB to include as part of audited annual financial statements.

Clarification of the separation and distinction of Debt Service Reserve Funds (DRF) for loans secured by property tax revenues and loans secured by other revenues. The FNFA has been given flexibility to withhold between 1-5% of the loan amount, depending on the circumstances and in accordance with regulations. Initially, the withheld rate was set at 5%, at a higher threshold than observed in municipal borrowing practices. Some flexibility was granted with this change, but the Authority’s practices are expected to remain unchanged. Clarification was also given that only Borrowing Members who have received financing can be called on to contribute to or replenish a DRF and only the DRF for their borrowing stream. There are two streams, one for Property Taxation and the other for Other Revenues. In each stream, however, Borrowing Member obligations to replenish are joint and several. Enhancement to the Act also established that the FNFA’s priority over other creditors of a First Nation in the event of an insolvency arises from the date the borrowing member has received financing from the FNFA, thus strengthening its priority.

The ability to invest sinking fund proceeds in FNFA bonds to reduce net funding costs, although, from a ratings perspective, this does not reduce the total amount of outstanding debt. The increased flexibility will also allow FNFA to manage its bonds in the secondary markets.

Introducing a mechanism for repayment to the Credit Enhancement Fund (CEF), within 18 months, where the CEF has been used to replenish a DRF.

Credit Underwriting Process and Experience

This credit history of lending to First Nations through the First Nations Finance Authority is short as it only came into existence in 2006. More history can be found in the bank lending sector of making loans on First Nations reserves. There has not been a recorded loan default by a First Nation since at least 1970. There have been only a few known cases in the past where there was difficulty in collecting but, in those cases, either the financial institution failed to follow its own normal lending criteria or failed to properly contractually secure its position including the ‘Redirection to Pay’. Banking lenders have often noted strong moral suasion and moral obligation to fulfill loan repayment requirements due to the closeness of First Nations Communities and a sense of duty and honour. We highlight that FNFA’s experience to date shows a meaningful percentage of First Nations making payments ahead of schedule. In FNFA’s 2016 Annual Report, the level of prepayments is shown at $5.8mln, almost a full year’s interest payment ahead.

The financial strength and economic potential of First Nations communities continues to evolve in a constructive manner as evidenced by the number of First Nations that are participating in the First Nations Fiscal Management Act (FNFMA) and the growth in their own-source revenue. A total of 13 First Nations opted to participate in the FNFMA shortly after it came into force in April 2006 (i.e. original members). Today, there are 200 First Nations scheduled versus 634 First Nations across Canada.

It is estimated by Dr Dominique Collin of Waterford Strategies that own-source revenues accounted for about one-third of total revenues of participating First Nations combined, or $2.6bln, in Fiscal 2014-15. This is up from about 16% 10 years ago.

FNFA’s mandate allows First Nations to access ‘Long-Term Loans’ or financing that is supported by two types of revenue streams: property taxation revenues and other revenues. It also offers ‘Interim Financing Loans’ to cover costs during construction or bridge financing until FNFA issues its next debenture. FNFA has yet to receive a loan application which falls under the property taxation revenue stream, although the legislation was originally contemplated for this type of borrowing.

Long-term financing or lease financing of capital assets is made for the provision of local services on reserve bands. Short-term financing for operating or capital purposes is made either in accordance with the stated purposes of paragraph 5(1)(b) of the FNFMA which relates to spending supported by Property Tax Revenues or to refinance short-term debt incurred for capital purposes. The Other Revenues Regulation outlines spending purposes for Other Revenues (i.e. infrastructure, social and economic, land purchases, etc.).

FNFA’s ratings are constrained to the upside by a lack of diversity in size, credit quality and geographic diversification of its loan portfolio. Rating agencies have taken a cautious approach to rating the FNFA given its short operating history, rapid loan growth and loan concentration issues; but these overall characteristics are expected to strengthen over time as the program grows and expands across Canada. FNFA projects its loan portfolio to grow from about $297mln today to over $1.2bln by 2021 (Loan Growth: 2017 projected to $385mln; 2018 $515mln; 2019 $715mln; 2020 $955mln; 2021 $1.225bln).

As a matter of practice to ensure adequate diversification and to support its strong credit ratings, the FNFA has reduced its individual loan exposures with the goal of keeping concentrations below 20%. In 2014, Membertou (largest borrower) was 24.59% of the loan pool. In July 2016, it was down to 11%.

FNFA aspires to stronger geographical distribution as currently its members are located in only eight provinces. FNFA Board Policy for minimum Debt Coverage Ratio (‘DCR’) of its individual Borrowing Member loans is set to at least 1.23 times, but its members are operating at much higher thresholds. While Borrowing Members must meet stringent requirement to participate in the program already, the Authority limits their borrowing to 75% of their calculated borrowing capacity (75% Rule). Should a member want their loan amount to exceed 75%, the FNFA staff do a further review of financial information/revenue stream documents before granting such loan privileges.

Borrowing Member loans are all in Canadian dollars and are amortizing, but have loan terms that expire ahead of full amortization and therefore must be refinanced. FNFA’s borrowings are done in Canadian dollars, hence there is no foreign exchange risk assumed.

With respect to the amortization of client loans and refinancing risk, 90% of client loans have repayment terms that extend beyond FNFA’s debenture maturity in 2024. These clients are given a choice to lock-in rates with an interest rate swap for their full loan term, but none have taken this since Supreme Court decisions in respect of First Nations entitlements have caused revenues to grow much faster than the national average of revenue growth for First Nations (up 2.5 times since 2005) and, therefore, First Nations generally want the option to fully payout their loans in 2024. Of those First Nations that do not payout the loan and need to refinance, because FNFA operates under a sinking-fund approach with debt service collected to include principal along with interest, any amounts refinanced would approximate 50% of the original balance. Thus, interest rates would have to double to maintain the same annual interest commitments for FNFA’s clients.

Currently, the majority of FNFA’s intercepted revenues are from federal and provincial grants or revenue sharing arrangements, accounting for approximately 70% of total intercepted revenues. Some risks exists with respect the cyclicality of these revenue streams or other credit factors, but in general, these are well secured. As FNFA’s intercepted revenue stream contains a significant percentage of other revenues (i.e. non-government), normal credit risk factors apply. Today, business revenues include lease contracts from owned buildings that are anchored by strong national tenants. There is also a gaming business. The only existing pipeline and utility related revenues are associated with BC Hydro, Hydro Quebec and Hydro One which are provincial crowns.

In 2014-2015, the FNFA’s intercepted revenues had an Interest Rate Coverage Ratio (‘IRC’) of 6.3 times (i.e. revenues intercepted were 6.3 times greater than the debenture’s interest liability). Approximately 75% of these revenues were from federal/provincial revenue sharing agreements; the balance being contractual revenues, lease agreements and established Band businesses. At the time of the recent debenture issues, the percentage has fallen from 75% to 67%, but the coverage ratios have improved. Intercepted revenues are from Fed/Provincial sources alone have a Debt Coverage Ratio (‘DCR’) of 2.25 times annual debt service.

Interest Rate Coverage Ratio (‘IRC’) and Debt coverage Ratio (‘DCR’)

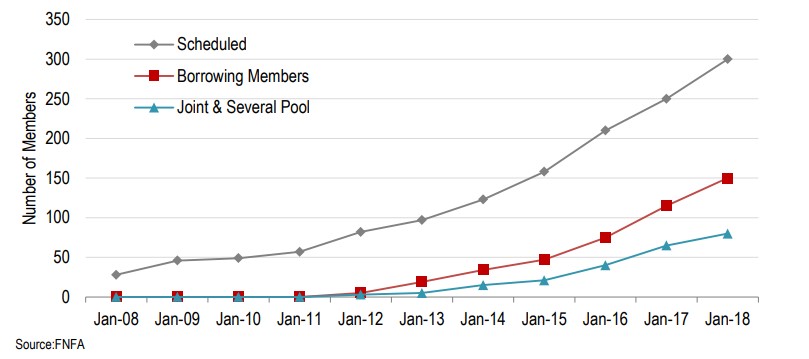

FNFA Borrowing Members, Future Projections

Financial Reporting and Transparency

Canada’s accounting architecture is founded on the work of several independent, volunteer bodies to establish authoritative standards of recommended or required practice. These bodies include the Public Sector Accounting Board (PSAB). PSAB issues standards and guidance with respect to matters of accounting (Public Sector Accounting Standards – PSAS), as well as financial reporting recommendations of good practice (Statements of Recommended Practice – SORPs). Their work is to serve the public interest by strengthening accountability in the public sector. The public sector refers to governments, government components, government organizations, and government partnerships. While compliance with PSASs is voluntary by the sovereign (Federal Government of Canada) and sub-sovereigns (Provinces), adherence to the PSAB requirements is legally required at the municipal level under various municipal acts. As it pertains to First Nations and their right to self-govern, reporting and transparency is voluntary by opting to participate under the First Nations Transparency Act and report under PSAB.

Successful monitoring of participating First Nations by the First Nations Finance Authority is dependent on access to financial information. The First Nations Transparency Act requires that each First Nation to which the Act applies publish on its Internet site, or cause to be published on an Internet site, the following documents within 120 days after the end of each financial year:

its audited consolidated financial statements

the Schedule of Remuneration and Expenses

the auditor’s written report respecting the consolidated financial statements; and

the auditor’s report or the review engagement report, as the case may be, respecting the Schedule of Remuneration and Expenses

These documents must remain accessible to the public on an internet website, for at least 10 years.

The Act further states that the Minister of Aboriginal Affairs and Northern Development must publish these same documents on the departmental website “without delay after the First Nation has provided him or her with those documents or they have been published.” First Nations do not have interim reporting requirements.

With respect to the First Nations Finance Authority, it has to file an annual report before July 31 of each year, within 120 days after year end (Section 88 of the Act). There are no interim reporting requirements, but Management is actively engaged in providing investors with regular updates.

First Nations Finance Authority

Financial Reporting and Transparency

Canada’s political system is a Westminster-style democracy with a federal system of parliamentary government. Canada is a constitutional monarchy in which the Queen or King is recognized as the head of state. Since February 6, 1952, the Canadian monarch has been Queen Elizabeth II, who is represented by the Governor General. The federal system is a union of partially self-governing regions, known as provinces (i.e. sub-sovereigns), under a central (federal) government (i.e. sovereign) where there is a division of power between the federal government and the provinces.

Canada has three main levels of government: federal, provincial (and territories), and municipal. The Constitution Act, signed in 1867, defines their respective powers, some of which are shared. While territories and municipalities have their own governments, they are not considered sub-sovereigns as they have no legislative authority to determine their powers and responsibilities. The responsibilities of the three territories are granted to them by the federal government while the responsibilities of municipal governments are granted by their respective provincial governments.

Under the constitution, the federal government has jurisdiction over: national defence, foreign affairs, employment insurance, banking, federal taxes, the post office, fisheries, shipping, railways, telephones, pipelines, aboriginal lands and rights, and criminal law. The federal government re-distributes wealth among the provinces through a system of equalization payments (i.e. extra money) given to provinces that are less wealthy, thus ensuring that the standards of health, education and welfare are the same for every Canadian.

The provinces have powers over: direct taxation, health care, prisons, education, some natural resources, marriage, road regulations and property and civil rights. Power over agriculture and immigration is shared between the federal and provincial governments.

Municipalities are responsible for areas such as libraries, parks, community water systems, local police, roadways and parking, receive their authority from the provincial governments. Across the country there are also band councils, which govern First Nations communities.

These elected councils are similar to municipal councils and make decisions that affect their local communities and operate under a framework of right to self-government or self determination. Aboriginal self-government is specifically referred to governments designed, established and administered by Aboriginal peoples under the Canadian Constitution through a process of negotiation and, where applicable, the provincial or territorial government.

History of Canada’s First Nations

According to the last census (2011), there were approximately 1.4 million indigenous people living in Canada (status and non-status), representing just over 4% of Canada’s 34.3 million population at that time. The indigenous count included 851,000 First Nations, 451,000 Métis, and 59,000 Inuit. A Canadian status indigenous person is a legal term referring to any First Nations individual who is registered with the federal government or a band which signed a treaty with the Crown. Many indigenous First Nations Canadians live on reserves, an area of land in which the legal title is held by the Crown, but is set apart for the use and benefit of a First Nations band.

First Nations lived in Canada for thousands of years before the arrival of the Europeans in the eleventh century. These First Nations were able to satisfy their material and spiritual needs through the resources of the natural world surrounding them. Historians tend to group Canada’s First Nations into six main geographic areas of the country as it exists today:

Woodland First Nations, who lived in dense boreal forest in the eastern part of the country

Iroquoian First Nations, who inhabited the southernmost area, a fertile land suitable for planting corn, beans and squash

Plains First Nations, who lived on the grasslands of the prairies

Plateau First Nations, whose geography ranged from semi-desert conditions in the south, to high mountains and dense forest in the north

Pacific Coast First Nations, who had access to abundant salmon and shellfish and gigantic red cedar trees used for building houses

First Nations of the Mackenzie and Yukon River Basins, whose harsh environment consisted of dark forests, barren lands, and the swampy terrain known as muskeg

Within each of these six areas, First Nations had very similar cultures, largely shaped by a common environment. They tended to function on the basis of a complex system of government based on democratic principles.

Today, the relationship between First Nations and the government is based on a broad collection of treaties covering pre-confederation, peace, and friendship treaties, as well as post-confederation or numbered treaties. In more recent history, there are also ‘Modern Treaties’, with the first one historically documented in the mid-1970s. Modern treaties have been entered into to satisfy comprehensive or specific land claim rights of Aboriginals that were not addressed by previous treaties, or by other legal means.

Aboriginal peoples, under the treaties, are recognized as the descendants of the original inhabitants of North America. The Canadian Constitution recognizes three groups of Aboriginal people with unique heritages, languages, cultural practices and spiritual beliefs. These are the Indians, Métis and Inuit. The term ‘First Nation’ came into usage in the 1970s and is widely used today to replace the word ‘Indian’ or ‘band’, although it is not a term that is legally recognized.

An historic Canadian settlement in the right to self-government was achieved in 2006, after 16 years of legal negotiations challenging the authority of the federal government. The agreement resulted in the transfer of $350mln in energy royalties to the Samson Cree. The money was placed in an independent trust fund (‘Kisoniyaminaw Heritage Trust’). It was the first time an Indian group was successful in seizing its own moneys and setting up a trust to which it had power of trustee and control of its own assets. The settlement also saw the removal of the federal government as trustee of all energy royalties for the Samson Cree and Ermineskin, two bands located on the Hobbena reserve in central Alberta.

“Control of our heritage trust moneys is a major step forward for the present and future generations of Samson Cree Nation members, and an important recognition of our Treaty 6 rights,” said Chief Victor Buffalo.

First Nations Finance Authority Issues its Largest Bond to date

Westbank, British Columbia (June 1, 2016) – The First Nations Finance Authority has issued its largest to date bond at $110 Million. The bond was purchased by 22 institutional investors in the global financial markets. It is FNFA’s 3 rd such debenture since 2014, bringing the total debt issued by FNFA up to $250 million, and will improve housing, infrastructure and economies on 29 First Nations across Canada. The bonds are backed by First Nations “Own Source Revenues” which are stable, predictable revenues self generated by the First Nation government through revenue sharing agreements with municipal, provincial and federal governments, as well as lease contracts, royalties, rents, and businesses revenues.

“The FNFA has received widespread acceptance from both the Capital Markets and First Nations,” confirms Ernie Daniels, President and CEO. “We now have a larger membership, greater geographical dispersion, and are financing projects across sectors such as public infrastructure, housing, green energy and other economic development initiatives. Our process is working and our track record proves it.”

197 First Nations across Canada have opted into the First Nations Fiscal Management Act, signifying their desire to join the FNFA. To date, 52 First Nations from 7 different provinces have completed FNFA’s steps-to-membership; the balance are working to complete these steps. Since FNFA’s first loan was issued in 2012 there has never been a late payment or a default on payment.

“The FNFA has experienced tremendous growth since our inaugural 2014 debenture,” states FNFA Deputy Chair Chief Joseph Bevan of Kitselas First Nation. “We have more First Nations participating, more projects being financed, and more investors buying our bonds.”

The FNFA is a not-for-profit First Nation institution established pursuant to the federal First Nations Fiscal Management Act, that provides any qualifying First Nation from across Canada with access to the capital markets. The First Nations govern the FNFA, as members elect from amongst themselves a Board of Directors.

FNFA facilitates loans to Borrowing Members from the proceeds of bond issuances. These loans can have repayment terms up to 30 years and offer fixed-rate options to assist the member First Nation’s budgeting needs. In order to fund member’s borrowing requirements prior to an expected bond issuance date, the FNFA also offers short-term loans at below Bank Prime. Shortterm loans are rolled over into each new bond. As more First Nations qualify to become Borrowing Members, the FNFA will continue to grow and diversify, looking to strengthen its credit rating and consequently the financial benefits to its members.

“The FNFA weaves together the needs of First Nations and Capital Markets,” explains Daniels. “First Nations need improvements to infrastructure, housing and economies and the Capital Markets require certainty of repayment. The FNFA is bridging the gap and allowing both sides to meet in the middle.”

The Board of Directors, membership and staff of the FNFA looks forward to continuing its work with First Nations governments from coast to coast to coast.

For More Info: Ernie Daniels President and CEO First Nations Finance Authority PH: (250) 768-5253 Fax: (250) 768-5258 info@fnfa.ca

Purchase includes lands formerly known as Bamberton

July 16, 2015, Malahat Nation (Coast Salish Territories), BC – The Malahat Nation, located next to the Vancouver Island town of Mill Bay, BC (40 Km north of Victoria, BC), has announced the purchase of approximately 525 hectares of land adjacent to their property, the area formerly known as Bamberton and including Oliphant Lake, more than tripling the size of their lands.

The land purchase is unique in British Columbia, with the Malahat Nation’s Chief, Council, Chief Executive Officer Lawrence Lewis and Chief Legal Officer Nicole Hajash undertaking the negotiations between the sellers and First Nations Finance Authority (FNFA). The purchase negotiations took more than 13 months to complete and is part of a larger Malahat Nation building plan, endorsed by the Nation community, Chief and Council.

“Today marks a monumental moment for the future of the Malahat Nation as this land purchase helps to restore more of our traditional lands into our stewardship,” says Chief Michael Harry, Malahat Nation. “We are moving forward to develop and protect the long-term viability of our people and our lands, while respecting our relationship with the neighbouring communities of southern Vancouver Island.”

The Malahat Nation plans to explore long-term opportunities for the newly acquired lands, including marine and terrestrial development, which align directly with its existing zoning and purpose. In consultation with Chief and Council, the Malahat Nation, through its Business Development Corporation plans to pursue a number of possible business development opportunities and joint ventures, including tourism, light industry, housing, and maritime development opportunities throughout the core of its land holdings. The land expansion opportunity was identified as part of the Malahat Nation Comprehensive Development Plan (CDP), which was first conceptualized in 2013 and officially came into effect earlier this year. The CDP created a vision for the Nation that focuses on long-term economic goals to improve the well-being of the Nation and its people.

The land purchase will also help to expand the Malahat Nation’s relationship with Quantum Murray, an industrial and environmental management services company with operations across Canada. In 2014, the Malahat Nation and Quantum Murray formed a joint venture to help pursue industrial service opportunities. Quantum Murray is currently employing members of the Malahat Nation as part of its development site on Malahat Reserve Lands.

“We are excited to be able to explore both short-term and long-term economic development initiatives,” says Lewis.”

In addition to the CDP, the Malahat Nation developed a Comprehensive Community Plan (CCP) in 2012 to act as the Nation’s governing plan and guiding principles and values. It is designed to help the Malahat Nation further exercise their sovereignty and make progress toward a future that incorporates social, economic, political, cultural growth, and wealth. As part of the CCP, the Malahat Nation identified the need for improved housing, helping to encourage members to return home and enhance the well being of their residents. In the last three years, nine new residences have been constructed, with four under construction, and plans for five to be built each year for the next five years. The Kwunew Kwasun Cultural Resource Centre was completed in 2014 and provides a place for the community to learn, share their values, re-build the strengths of their culture and have a space to gather.

About the Malahat Nation

The Malahat Nation is located adjacent to the town of Mill Bay, BC, 40 Km north of Victoria, BC. With close to 300 members in total – and 135 living on the Malahat lands – the Malahat Nation is a small First Nations community. Its Chief & Council are committed to improving the livelihood of their people through a series of initiatives based on comprehensive community and development plans that are focused on Nation building. For more information, visit www.malahatnation.ca and www.nationbuilding.ca.

-30-

Media contact:

Brian Cant, Tartan Group: 250-592-3838, 250-888-8729 (cell) or brian@tartangroup.ca